Piyush Gupta 16 Dec, 2024

At what age should you start saving for retirement?

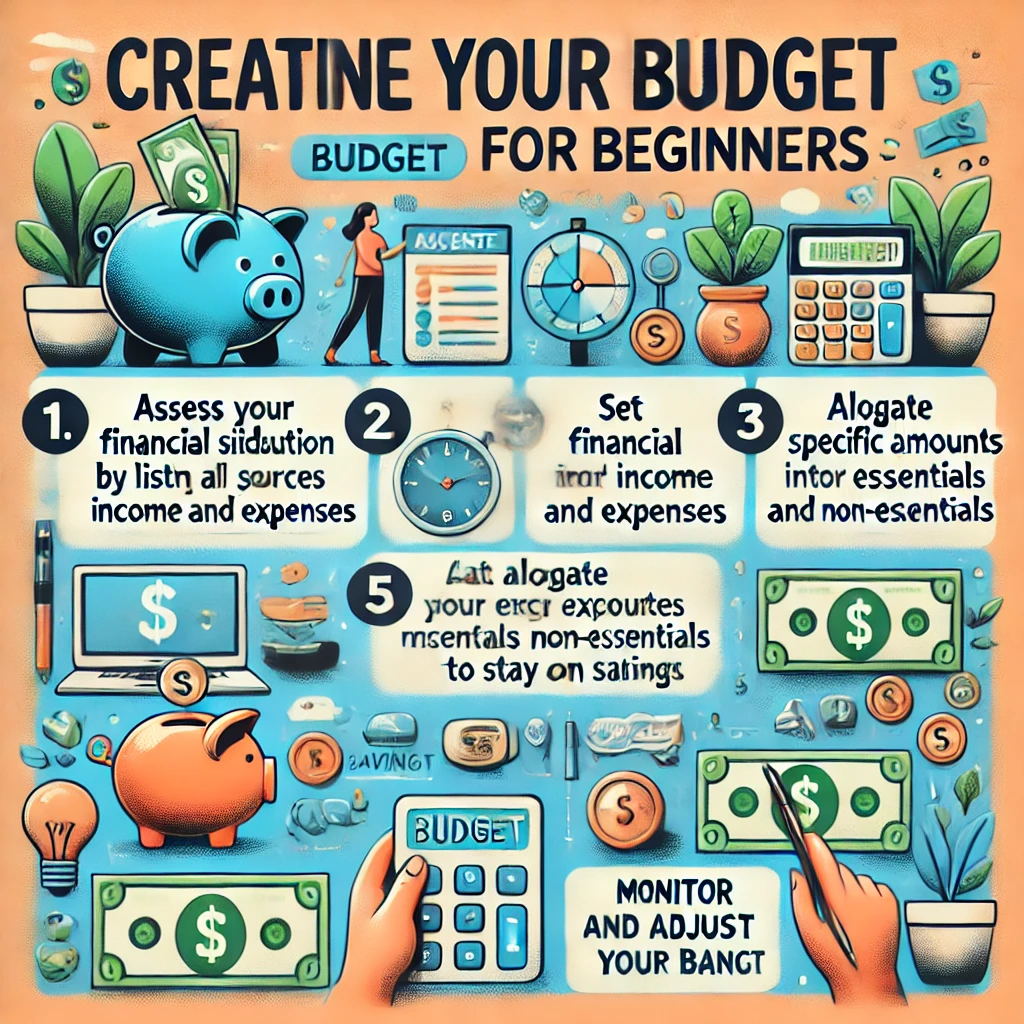

The best time to start saving for retirement is as early as possible, ideally in your 20s when you begin earning an income. Starting early provides several key benefits:

1. The Power of Compound Interest

- Compound interest allows your money to grow over time, as you earn returns not only on your contributions but also on the returns already accumulated.

- For example, saving $200 a month starting at age 25 could grow to significantly more than starting the same amount at age 35, even if the total contributions are the same.

2. Smaller Contributions Over Time

- Starting early means you can save smaller amounts consistently over a longer period, making it more manageable to reach your retirement goals without a significant financial burden.

3. Building Good Financial Habits

- Starting early helps instill a habit of saving, which can lead to better financial discipline and planning.

What If You Start Later?

If you can’t start saving in your 20s, start as soon as possible. For those starting later:

- Save more aggressively.

- Take advantage of employer-sponsored plans like 401(k)s or government-matched contributions.

- Delay retirement if needed to allow your savings to grow.

General Recommendation by Decade:

- 20s: Save at least 10-15% of your income, including employer matches.

- 30s: If you haven’t started, aim to contribute 15-20% of your income to make up for lost time.

- 40s and beyond: Maximize retirement contributions and catch-up contributions if available.

The earlier you begin, the more time you give your investments to grow, reducing the financial pressure later in life.