Piyush Gupta 15 Nov, 2024

How Do You Set and Achieve Financial Goals?

Setting and achieving financial goals involves a clear process of planning, execution, and tracking. Here's a step-by-step guide to help you get started:

1. Define Your Financial Goals

- Be Specific: Clearly state what you want to achieve, e.g., "Save $20,000 for a down payment on a house within three years."

- Categorize Goals: Split your goals into short-term (less than a year), medium-term (1-5 years), and long-term (5+ years). Examples:

- Short-term: Build an emergency fund.

- Medium-term: Pay off credit card debt.

- Long-term: Save for retirement.

2. Make Goals SMART

- Specific: Know exactly what you want to achieve.

- Measurable: Quantify your goals (e.g., save $500/month).

- Achievable: Set realistic objectives based on your income and expenses.

- Relevant: Align goals with your life priorities.

- Time-bound: Set deadlines to create urgency.

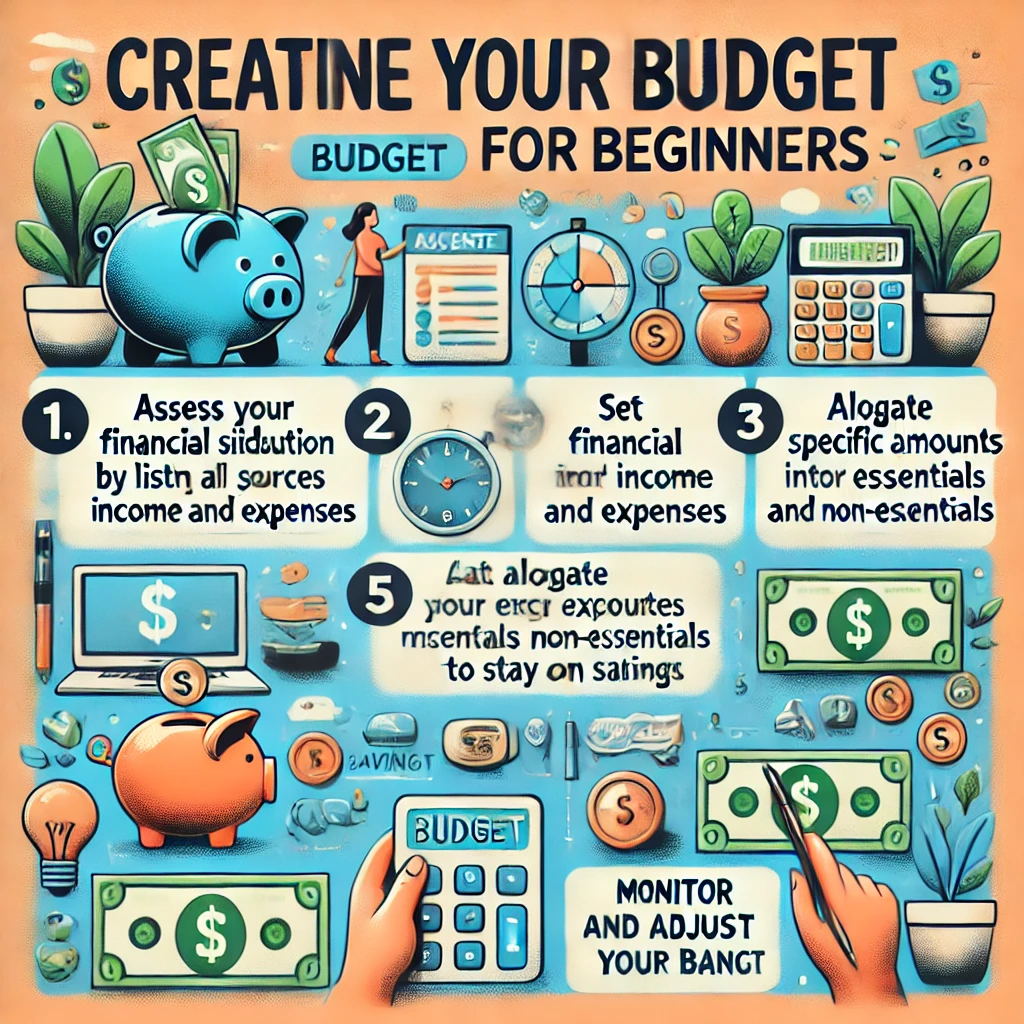

3. Assess Your Financial Situation

- Review your income, expenses, and savings.

- Calculate your net worth (assets minus liabilities).

- Identify areas where you can reduce spending or reallocate funds toward your goals.

4. Create a Budget

- Use the 50/30/20 Rule: Allocate 50% of your income to needs, 30% to wants, and 20% to savings or debt repayment.

- Track expenses to find opportunities for saving.

5. Break Down Goals into Smaller Milestones

- Divide big goals into manageable steps. For instance, if your goal is to save $12,000 in two years, aim to save $500 per month.

- Celebrate milestones to stay motivated.

6. Choose the Right Tools and Strategies

- Savings Accounts: For emergency funds or short-term goals.

- Investment Accounts: For medium- and long-term goals, consider stocks, bonds, or mutual funds.

- Debt Repayment Plans: Use strategies like the snowball (smallest balance first) or avalanche (highest interest first) method to pay off debt.

- Use budgeting apps to track progress (e.g., Mint, YNAB).

7. Automate Your Savings

- Set up automatic transfers to savings or investment accounts.

- Automating reduces the temptation to spend and ensures consistent progress.

8. Monitor and Adjust Regularly

- Review your goals and financial situation periodically.

- Adjust for changes in income, expenses, or unexpected events.

- Reassess goals to ensure they remain relevant and achievable.

9. Seek Professional Guidance

- Consult financial advisors or planners if you need help creating or managing a financial plan.

- They can provide tailored advice for investments, retirement, or estate planning.

10. Stay Committed and Patient

- Financial goals often take time. Stay focused and avoid impulsive decisions.

- Remember that small, consistent steps lead to significant results.

By following this structured approach, you can set clear financial goals and take practical steps to achieve them, ensuring a more secure and fulfilling financial future.