Piyush Gupta 07 Aug, 2024

How Can You Manage Debt Effectively?

Managing debt effectively involves a combination of strategic planning, disciplined financial habits, and informed decision-making. Here are some key steps to help you manage debt effectively:

1. Assess Your Financial Situation

- List All Debts: Make a detailed list of all your debts, including credit cards, student loans, car loans, and mortgages. Include the interest rates, minimum payments, and due dates for each.

- Calculate Total Debt: Determine your total debt amount to get a clear picture of your financial obligations.

- Review Your Income and Expenses: Evaluate your monthly income and expenses to understand your cash flow and identify areas where you can cut back.

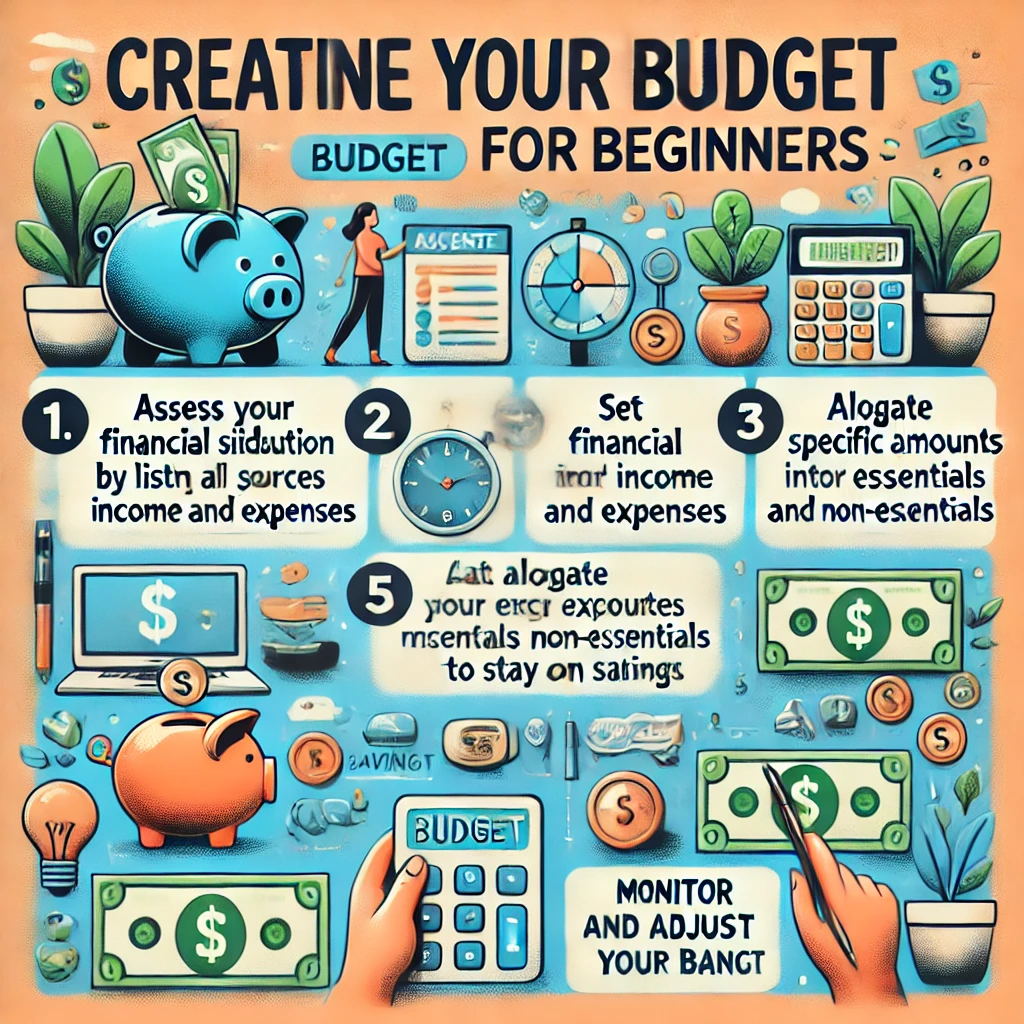

2. Create a Budget

- Set Financial Goals: Establish clear, realistic financial goals, such as paying off a specific debt or saving a certain amount each month.

- Track Spending: Use budgeting tools or apps to track your spending and ensure you stay within your budget.

- Prioritize Expenses: Focus on essential expenses like housing, utilities, and groceries, and reduce discretionary spending.

3. Develop a Debt Repayment Plan

- Debt Snowball Method: Focus on paying off the smallest debts first while making minimum payments on larger debts. This can provide quick wins and motivation.

- Debt Avalanche Method: Prioritize paying off debts with the highest interest rates first, which can save you money in interest over time.

- Consolidate Debts: Consider consolidating high-interest debts into a single loan with a lower interest rate, which can simplify payments and reduce interest costs.

4. Negotiate with Creditors

- Lower Interest Rates: Contact creditors to negotiate lower interest rates, especially if you have a good payment history.

- Payment Plans: Ask creditors if they offer payment plans or hardship programs that can make payments more manageable.

5. Increase Income

- Side Hustles: Consider taking on a part-time job or freelance work to boost your income.

- Sell Unneeded Items: Sell items you no longer need through online marketplaces or garage sales to generate extra cash.

6. Build an Emergency Fund

- Save Regularly: Set aside a small amount each month for an emergency fund to cover unexpected expenses, which can prevent further debt accumulation.

- Aim for 3-6 Months of Expenses: Ideally, your emergency fund should cover 3-6 months of living expenses.

7. Avoid Accumulating More Debt

- Limit Credit Card Use: Use cash or debit cards for purchases to avoid accruing more credit card debt.

- Think Before Borrowing: Consider the necessity and impact of taking on new debt before making a decision.

8. Seek Professional Help

- Credit Counseling: Consult a certified credit counselor for advice and personalized debt management plans.

- Debt Management Programs: Enroll in a debt management program if necessary, which can help you consolidate and pay off debts under professional guidance.

9. Stay Informed and Motivated

- Educate Yourself: Read books and articles on personal finance to improve your financial literacy.

- Celebrate Milestones: Reward yourself for reaching debt repayment milestones to stay motivated.

10. Review and Adjust Regularly

- Monitor Progress: Regularly review your debt repayment plan and budget to ensure you are on track.

- Make Adjustments: Be flexible and willing to adjust your plan as your financial situation changes.