Piyush Gupta 14 Sep, 2024

What Are the Financial Planning Basics for the Self-Employed?

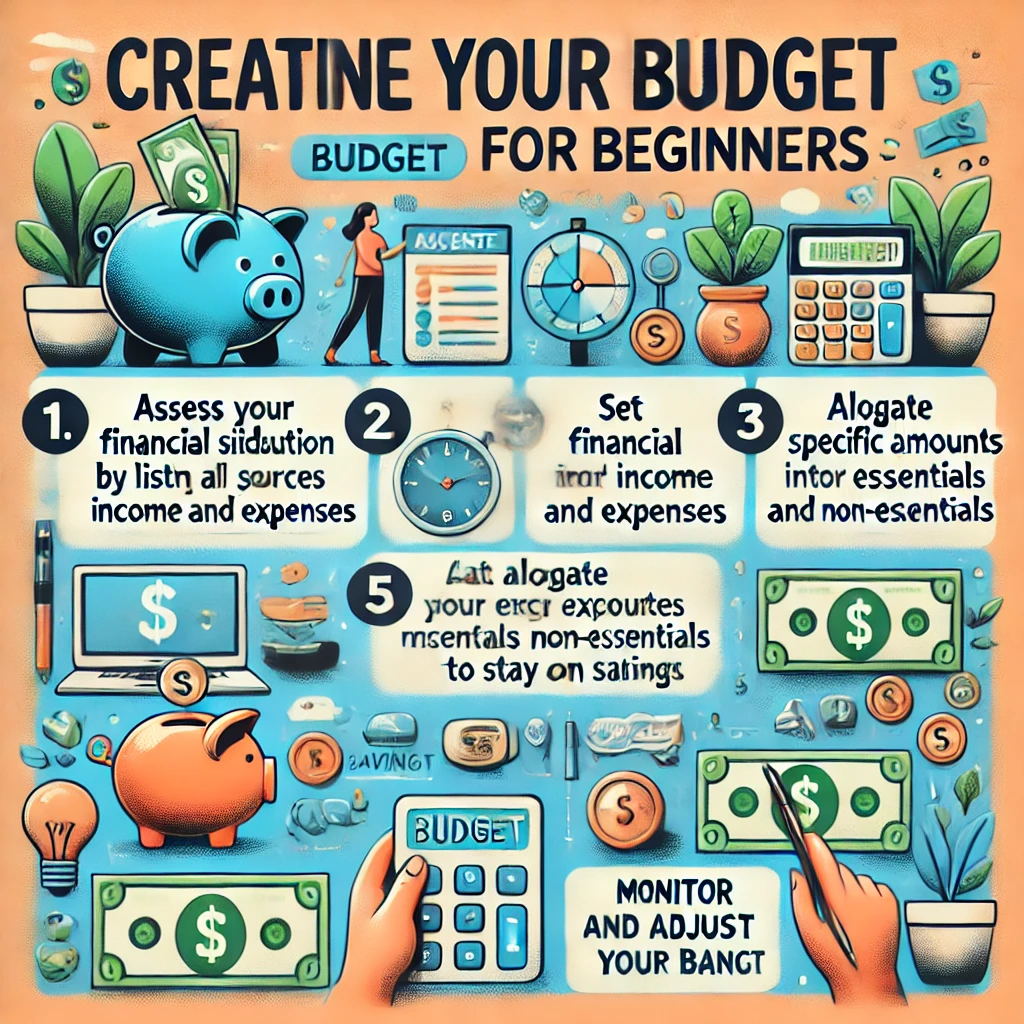

Financial planning for the self-employed is crucial, as it often requires more proactive management than traditional employment due to fluctuating income, tax responsibilities, and lack of employer-provided benefits. Here are the basic steps:

1. Budgeting and Managing Cash Flow

- Track Income and Expenses: Keep detailed records of your earnings and expenditures to manage the variability in income.

- Separate Business and Personal Finances: Open a separate bank account for your business to simplify accounting and tax reporting.

- Build an Emergency Fund: Because income may fluctuate, aim to save 3-6 months’ worth of living expenses to cover slow periods or unexpected costs.

2. Tax Planning

- Estimate Quarterly Taxes: Self-employed individuals are responsible for paying taxes quarterly, including income tax and self-employment tax (which covers Social Security and Medicare).

- Deduct Business Expenses: Common deductions include office supplies, travel expenses, equipment, and home office expenses.

- Hire a Tax Professional: Consider hiring an accountant to help you with tax strategies, such as setting up a business structure (like an LLC) that may offer tax advantages.

3. Retirement Savings

- Open a Self-Employed Retirement Account: Options include SEP IRAs, SIMPLE IRAs, and Solo 401(k)s, which allow for high contribution limits and tax deferral.

- Contribute Regularly: Even with variable income, prioritize retirement savings. These contributions can also reduce taxable income.

4. Insurance Planning

- Health Insurance: Self-employed individuals need to secure their own health coverage. Look into private health insurance or marketplace options.

- Disability and Life Insurance: Protect yourself in case of illness, injury, or death, as there’s no employer to provide this safety net.

- Liability Insurance: Depending on your business, you may need professional liability, general liability, or product liability insurance.

5. Debt Management

- Avoid Excessive Business Debt: Only take on debt that can be easily repaid with expected income. Use debt strategically to invest in growth but avoid overextending yourself.

- Consolidate or Refinance: If debt is high-interest, consider consolidating or refinancing it for better rates.

6. Set Financial Goals

- Short-Term: Pay off business loans, save for taxes, and maintain cash flow.

- Long-Term: Build up retirement savings, set aside funds for business expansion, or aim for early financial independence.

7. Invest in Your Business

- Reinvest Profits: Use a portion of your earnings to improve your business, whether through marketing, new equipment, or hiring staff.

- Continue Learning: Take courses or attend workshops that enhance your skills, making you more competitive in your field.

8. Succession and Exit Planning

- Plan for the Future: Think about what happens if you want to retire or sell your business. Have a plan in place for either selling or transferring ownership.

Being self-employed requires a higher level of financial discipline and long-term planning to ensure both personal and business financial health.