Piyush Gupta 09 Dec, 2024

What are the key components of a solid financial plan?

A solid financial plan serves as a roadmap for achieving financial goals and managing resources effectively. Here are the key components:

1. Goals and Objectives

- Clearly define short-term, medium-term, and long-term financial goals (e.g., buying a house, saving for retirement, paying off debt).

- Ensure goals are SMART: Specific, Measurable, Achievable, Relevant, and Time-bound.

2. Net Worth Statement

- Assess current financial status by listing all assets (cash, investments, property) and liabilities (loans, credit card debt).

- Calculate net worth: Net Worth = Assets - Liabilities.

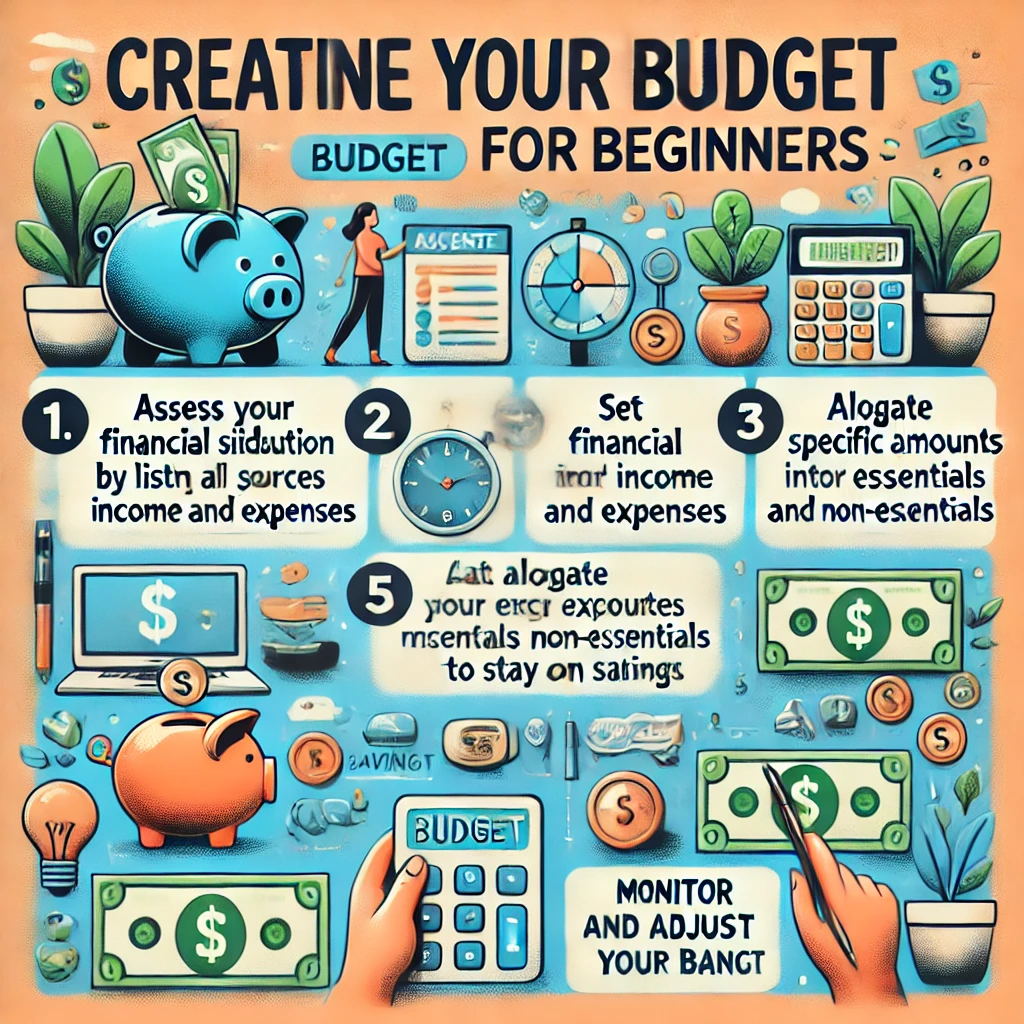

3. Budgeting and Cash Flow Management

- Track income and expenses to understand spending patterns.

- Create a budget to prioritize essential expenses, savings, and discretionary spending.

- Aim for a surplus to allocate towards savings and investments.

4. Emergency Fund

- Maintain 3–6 months’ (Instant Funds) of living expenses in an accessible, low-risk account for unexpected situations (job loss, medical emergencies).

5. Debt Management

- Evaluate existing debts and prioritize repayment (e.g., high-interest debts first).

- Plan for reducing or eliminating unnecessary debt over time.

6. Savings Plan

- Establish savings goals for various purposes, such as:

- Retirement

- Education

- Major purchases (e.g., a car or home)

7. Investment Strategy

- Determine risk tolerance and time horizon.

- Diversify investments across asset classes (stocks, bonds, real estate) to balance risk and returns.

- Regularly review and rebalance the portfolio.

8. Insurance Coverage

- Protect against unforeseen risks with adequate insurance:

- Health insurance

- Life insurance

- Disability insurance

- Property and liability insurance

9. Retirement Planning

- Estimate retirement needs and set contributions to retirement accounts (e.g., 401(k), IRA, or pension plans).

- Consider tax-advantaged investment options and employer matches.

10. Tax Planning

- Minimize tax liability by leveraging deductions, credits, and efficient investment strategies.

- Plan for year-end tax-saving opportunities and long-term strategies like Roth conversions.

11. Estate Planning

- Ensure assets are distributed according to your wishes through wills, trusts, and beneficiary designations.

- Consider powers of attorney and healthcare directives for end-of-life decisions.

12. Periodic Review and Adjustments

- Regularly review the plan to adapt to changes in income, expenses, goals, or market conditions.

- Update financial goals and strategies as life circumstances evolve (e.g., marriage, children, career changes).

13. Professional Guidance

- Seek advice from financial advisors, tax professionals, or legal experts for complex situations or specialized knowledge.

By integrating these components, a financial plan provides structure, ensures preparedness for uncertainties, and facilitates the achievement of long-term financial security.