Piyush Gupta 10 Dec, 2024

How can one effectively budget for short-term and long-term goals?

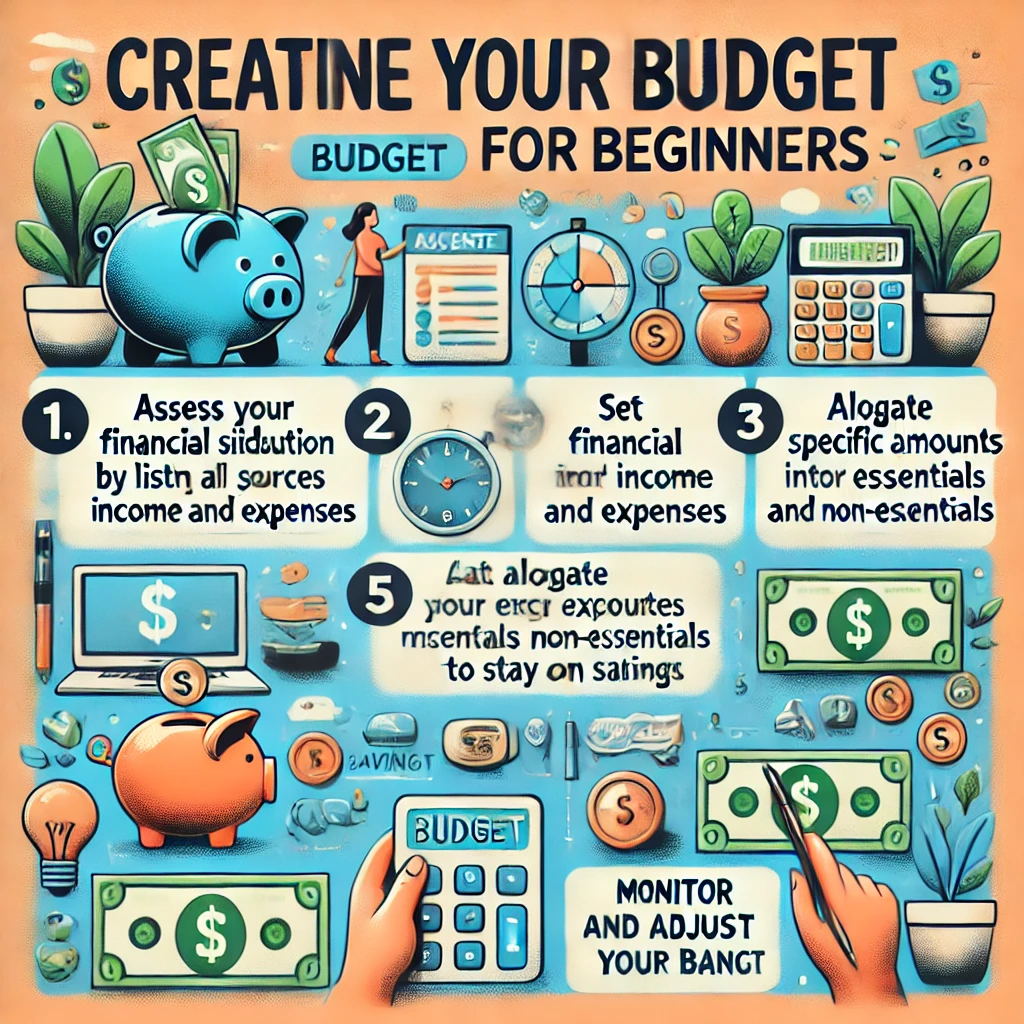

Budgeting for short-term and long-term goals requires a clear understanding of priorities, disciplined financial planning, and regular review. Here's a guide to effectively budget for both:

1. Define Your Goals

- Short-term goals: These are goals you aim to achieve within a year (e.g., saving for a vacation, paying off a small debt, or buying a new appliance).

- Long-term goals: These span several years, often five or more (e.g., buying a house, retirement, or funding education).

2. Assess Your Current Financial Situation

- List all income sources.

- Track your expenses to understand spending habits.

- Identify surplus income that can be allocated toward goals.

3. Prioritize Your Goals

- Rank your goals by urgency and importance.

- Decide which goals to focus on first, balancing short-term and long-term priorities.

4. Create a Budget Plan

- Fixed expenses: Allocate funds for necessities like rent, utilities, and insurance.

- Variable expenses: Include flexible spending categories such as groceries and entertainment.

- Savings for goals:

- Short-term: Open a high-yield savings account for quicker access and faster growth.

- Long-term: Use investment accounts, like a 401(k), IRA, or diversified portfolio.

5. Allocate Funds Strategically

- Follow a savings rule like the 50/30/20 rule:

- 50% for needs

- 30% for wants

- 20% for savings (split between short-term and long-term goals).

- Automate transfers to savings and investment accounts to ensure consistency.

6. Use Goal-Specific Accounts

- Create separate accounts for different goals to avoid mixing funds.

- Label each account clearly (e.g., "Emergency Fund," "Vacation Fund").

7. Leverage Tools and Resources

- Use budgeting apps or spreadsheets to track progress.

- Take advantage of employer-sponsored programs like retirement matching.

8. Regularly Review and Adjust

- Evaluate your budget monthly or quarterly to check progress.

- Adjust allocations if income or expenses change, or if goals shift.

9. Stay Flexible and Prepare for Emergencies

- Maintain an emergency fund with at least 3-6 months’ worth of expenses.

- Be ready to re-prioritize if unexpected expenses arise.

Example:

Goal: Save $10,000 for a down payment in 3 years while saving $2,000 for a vacation in 6 months.

- Monthly surplus: $800

- Short-term (vacation): Allocate $333/month for 6 months.

- Long-term (down payment): After the vacation is funded, increase contributions to $800/month for 30 months.

Effective budgeting combines planning, consistency, and adaptability to achieve financial goals without compromising your current lifestyle.