Piyush Gupta 19 Dec, 2024

How should your investment strategy change as you age?

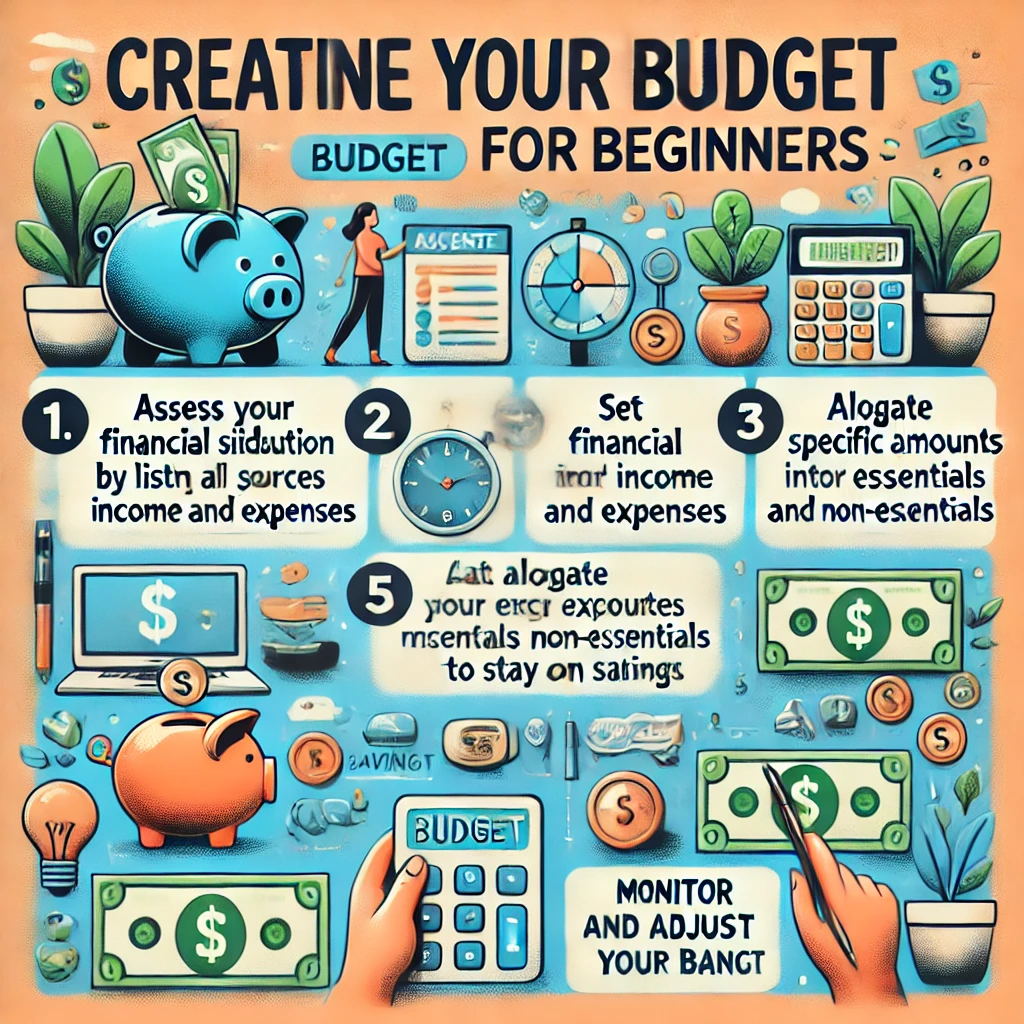

Your investment strategy should evolve as you age to align with your changing financial goals, risk tolerance, and time horizon. Here’s a general guide:

In Your 20s and 30s: Building Wealth

- Risk Tolerance: High. You have a long time horizon to recover from market downturns.

- Asset Allocation: Focus heavily on growth-oriented investments, such as stocks or equity-focused mutual funds and ETFs.

- Example: 80-90% stocks, 10-20% bonds.

- Goals:

- Maximize contributions to retirement accounts (e.g., 401(k), IRA).

- Build an emergency fund (3-6 months of living expenses).

- Start investing in tax-advantaged accounts and consider diversified index funds.

- Strategy: Dollar-cost averaging, leveraging compound interest, and tolerating market volatility.

In Your 40s: Balancing Growth and Stability

- Risk Tolerance: Moderate. You may start prioritizing preserving wealth while still seeking growth.

- Asset Allocation: Shift to a mix of growth and income-generating investments.

- Example: 60-70% stocks, 30-40% bonds.

- Goals:

- Accelerate retirement savings.

- Diversify your portfolio (e.g., adding real estate or dividend-paying stocks).

- Consider college savings plans if applicable.

- Strategy: Rebalance your portfolio annually to maintain desired allocations.

In Your 50s: Preparing for Retirement

- Risk Tolerance: Moderate to low. You’re nearing retirement and need to protect your savings from significant losses.

- Asset Allocation: Increase allocation to conservative investments like bonds or income funds.

- Example: 50-60% stocks, 40-50% bonds.

- Goals:

- Maximize contributions to retirement accounts, especially catch-up contributions if allowed.

- Reduce high-interest debt (e.g., credit cards).

- Plan for retirement income needs (e.g., health care, housing).

- Strategy: Stress-test your retirement plan to ensure it meets your expected expenses.

In Your 60s and Beyond: Preserving Wealth

- Risk Tolerance: Low. Focus shifts to preserving capital and generating steady income.

- Asset Allocation: Conservative allocation with a significant portion in fixed-income assets.

- Example: 30-40% stocks, 60-70% bonds/cash equivalents.

- Goals:

- Create a sustainable withdrawal strategy (e.g., 4% rule).

- Minimize taxes on withdrawals.

- Ensure sufficient liquidity for unforeseen expenses.

- Strategy: Monitor spending, reassess insurance coverage, and maintain diversification.

Additional Considerations Across All Ages

- Life Events: Adjust your strategy for major milestones (marriage, buying a home, etc.).

- Diversification: Maintain a well-diversified portfolio to manage risk.

- Rebalancing: Review and adjust your investments regularly.

- Professional Guidance: Consider working with a financial advisor as your portfolio and needs become more complex.

Would you like a deeper dive into any specific age group or investment type?