Piyush Gupta 26 Dec, 2024

How can parents financially plan for their children’s education?

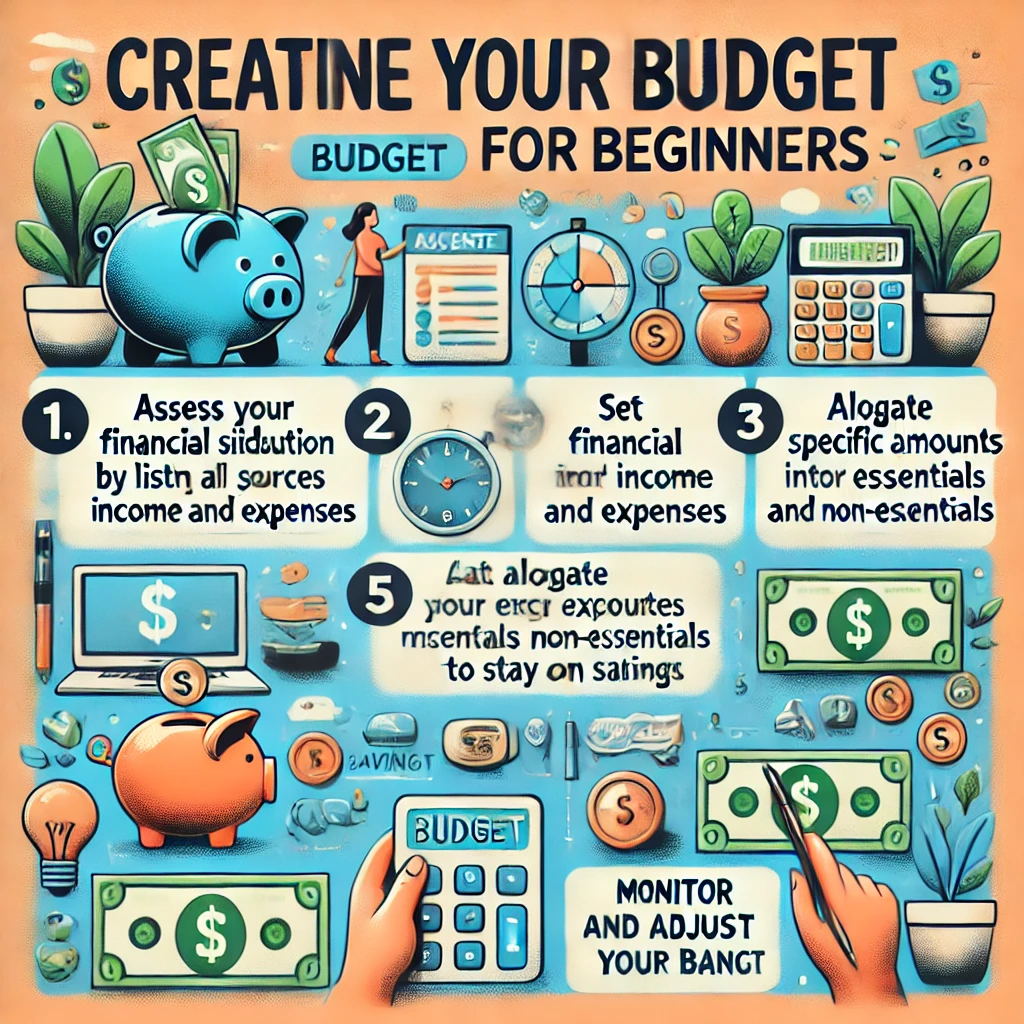

Financial planning for a child’s education is a critical step for parents to ensure they can support their child’s future academic goals without undue financial strain. Here are some practical steps parents can take:

1. Start Early

-

Compound Interest Advantage: The earlier you begin saving, the more you benefit from compound interest.

-

Set Realistic Goals: Estimate the future costs of education based on current tuition rates and anticipated inflation.

2. Estimate Costs

-

Research: Investigate tuition fees, living expenses, and other related costs for the types of schools or universities you envision (e.g., public, private, or international institutions).

-

Consider Inflation: Education costs typically rise faster than general inflation.

3. Choose the Right Savings Plan

-

529 College Savings Plans (U.S.): Tax-advantaged accounts specifically for education expenses.

-

Education Savings Accounts (ESAs): Offer tax-free growth if used for qualified educational expenses.

-

Fixed Deposits or Bonds: Provide guaranteed returns and low risk.

-

Investment Accounts: Higher risk but potential for greater long-term returns through stocks or mutual funds.

4. Diversify Savings and Investments

- Spread investments across multiple vehicles (e.g., savings accounts, stocks, bonds) to balance risk and return.

- Reassess and rebalance your portfolio periodically to align with your goals.

5. Explore Scholarships and Grants

- Research scholarship opportunities your child may be eligible for to reduce out-of-pocket expenses.

- Stay updated on financial aid options provided by schools and government programs.

6. Cut Costs Where Possible

- Consider community colleges for the initial years of education, transferring to a four-year institution later.

- Encourage part-time work or internships to help your child contribute financially plan and gain experience.

7. Involve the Whole Family

- Encourage grandparents or relatives to contribute to education savings as part of gifts or inheritance planning.

8. Plan for Contingencies

- Set up a contingency fund for unforeseen expenses related to education, such as travel or special projects.

- Purchase life insurance or critical illness insurance to ensure the child’s education is covered in case of emergencies.

9. Automate Savings

- Set up automatic contributions to dedicated education savings accounts to stay consistent with your financially plan .

10. Consult a Financial Advisor

- Seek professional advice to create a tailored education savings plan based on your income, expenses, and future goals.